What the Latest JOLTS Report Says About the 2025 Labor Market

After months of uncertainty due to the federal government shutdown, new labor market data is back in focus. Job openings remain elevated, hiring momentum is weak, and worker movement continues to slow. For employers heading into 2026, opportunities still exist, but progress is uneven, and risks are growing.

Building on reporting from HR Brew journalist Paige McGlauflin, the latest JOLTS report shows incremental movement rather than a meaningful rebound. Combined with the unemployment and payroll figures cited by Wall Street Journal journalists Deng, Torry, and Lahart, the U.S. unemployment rate rose to 4.6% in November, the highest level in more than four years, despite modest job gains.

The data provides important context for understanding the Job Openings and Labor Turnover Survey from the Bureau of Labor Statistics. When viewed together, the reports point to a labor market that appears stable on the surface but is increasingly constrained beneath the surface.

Job Openings Rise While Hiring Stalls

The latest JOLTS report shows employers reported about 7.7 million job openings in September and October, up from 7.2 million in August. While this increase interrupts the steady decline seen earlier in the year, it does not signal a return to aggressive hiring.

A labor economist at ZipRecruiter noted that the rise in openings could represent a slow pivot point for the labor market. However, they cautioned that upcoming reports will determine whether this increase reflects sustained demand or temporary distortions related to delayed data collection during the shutdown.

Job openings and hiring continue to move in opposite directions. Employers recorded 5.1 million hires in October, unchanged from August and 225,000 fewer hires than in September. The disconnect between available jobs and actual hiring suggests that many organizations remain cautious, constrained by cost pressures, policy uncertainty, or productivity concerns. The pattern aligns with WSJ reporting that many employers are delaying seasonal hiring and reassessing staffing needs amid weakening economic signals.

Why Job Openings Alone Do Not Tell the Full Story

For employers, job openings may create a false sense of optimism. Workers are more concerned with whether these roles become real opportunities than with the number of openings.

Chief Economist at Glassdoor, Daniel Zhao, emphasizes that stable openings without increased hiring reflect employer hesitation. Businesses are signaling demand but are reluctant to commit, creating frustration for job seekers and bottlenecks for operations teams.

Labor turnover continues to slow as a result. Employers reported 2.9 million quits in October, down 187,000 from September and 276,000 fewer than a year earlier. The decline suggests workers are staying in place not because of strong engagement, but because confidence in external opportunities has eroded.

At the same time, layoffs and discharges rose to 1.9 million in October, up 73,000 from September. While layoffs remain below recessionary levels, the upward trend reinforces the cautious posture many organizations have adopted. Employers are trimming selectively rather than expanding, contributing to a fragile labor market equilibrium.

Slowing Labor Turnover Creates Hidden Risks

Lower quit rates may seem positive, and many HR teams welcome reduced attrition. However, the latest JOLTS report and unemployment data suggest this stability may be masking deeper disengagement.

When workers stay primarily due to uncertainty, morale and productivity can suffer. Employees may limit discretionary effort, resist change, or avoid taking on additional responsibility. Over time, this creates operational drag that is harder to measure than turnover alone.

Zhao warns that if the labor market improves in 2026, employers could face a delayed wave of resignations. Employees who postponed job searches could leave quickly once confidence returns, straining operations and disrupting workforce planning.

Sector Specific Signals Worth Watching

Healthcare and social assistance, one of the strongest job growth sectors in recent years, showed notable divergence in the latest JOLTS report. Job openings in the industry rose by 49,000, but hires declined by 95,000 during the same period.

Quits in healthcare fell by 114,000 month over month, while layoffs increased to 184,000 in October. That figure represents an increase of 13,000 from September and 35,000 from August. While short-term changes do not confirm a downturn, the scale of these movements warrants close attention, given healthcare’s outsized role in overall labor market trends.

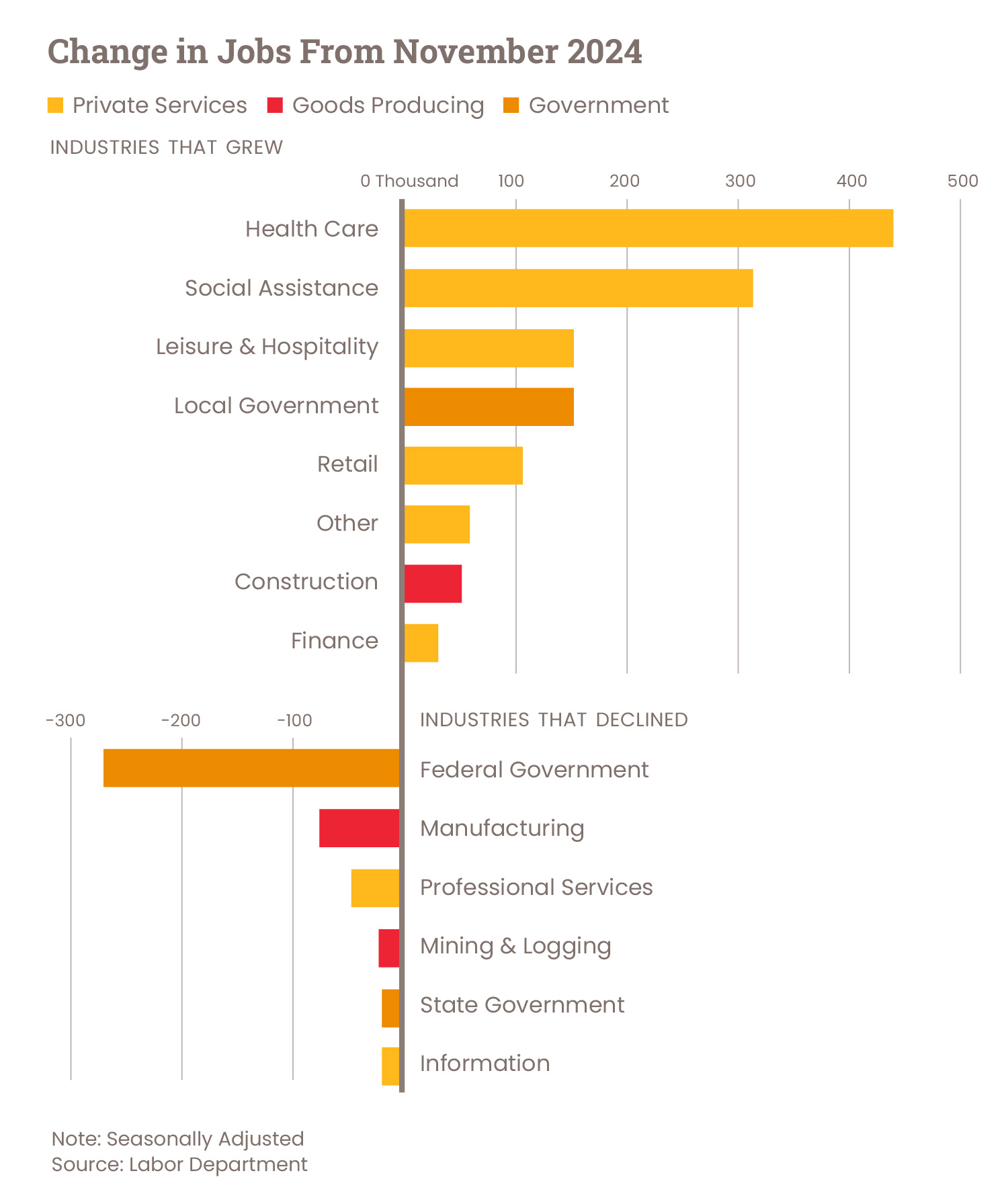

WSJ reporting reinforces this imbalance. While healthcare and education added roughly 128,600 private-sector jobs in October and November combined, manufacturing, transportation, warehousing, and temporary-help services shed jobs. Information and finance roles also declined, signaling weakness in traditionally stable white-collar sectors.

Federal government employment remains another pressure point. Payroll data shows federal employment shrank by 6,000 jobs in November, following a 162,000 job decline in October. Since January, federal employment has been down approximately 270,000, reaching its lowest level in more than a decade. These reductions reflect delayed impacts of layoffs, deferred resignations, and policy-driven workforce cuts.

Workforce Planning Challenges Are Intensifying

Looking at the broader picture, labor turnover in the US has stagnated in 2025. The unemployment rate rose from 4.4% in September to 4.6% in November, while job growth slowed to just 64,000 jobs in November after a loss of 105,000 in October. The economy has shed jobs in three of the past six months.

Economists now describe the labor market as a low-fire, low-hire environment. Companies are not laying off workers en masse, but they are also unwilling to hire aggressively. Demographic pressures, including retirements among skilled workers, continue to tighten labor supply, while skills mismatches limit how quickly employers can fill critical roles.

Wage growth has also slowed. Private-sector hourly earnings rose 3.5% year over year, the lowest rate outside pandemic distortions in several years. Combined with rising part-time underemployment and growing worker discouragement, this trend adds to broader workforce dissatisfaction.

Preparing for What Comes Next

The combined signals from the JOLTS report, unemployment, and payroll data reinforce a key reality for HR and operations leaders: stability today does not guarantee stability tomorrow. Organizations that prepare now will respond more effectively when hiring accelerates.

Preparation begins with efficient workforce planning. Leaders can streamline hiring, reduce barriers to internal mobility, and develop flexible labor models that adapt to changing demand. Investing in upskilling and technology also enables teams to do more with less.

As Jerome Powell recently noted, labor market measurement challenges may even be overstating job creation. That uncertainty makes operational agility even more critical.

Final Takeaways

The latest JOLTS report, backed by November employment data, paints a consistent picture. Job openings persist, hiring remains cautious, turnover is slowing, and unemployment is rising modestly. While the labor market appears calm, underlying pressures suggest future volatility.

For employers, now is the time to reassess workforce planning, strengthen engagement, and build systems that support flexibility. Decisions made today will shape organizational performance when conditions shift again.

Start Planning for Success

Schedule a demo with ShiftSwap™ today and learn how to streamline your workforce management.